probability mass function

Probability mass function

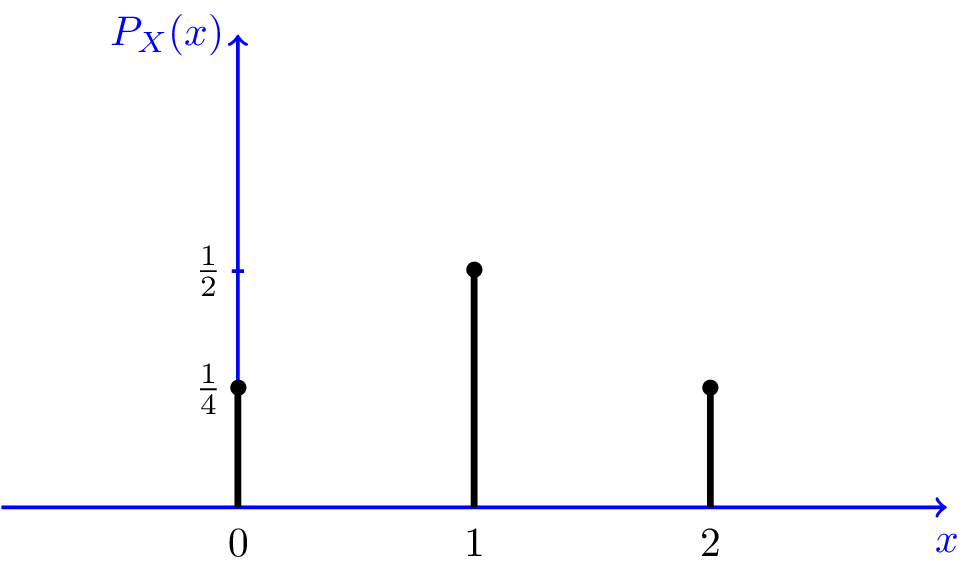

A probability mass function is a function that gives the probability that a discrete random variable is exactly equal to some value.

Definition

Probability mass function is the probability distribution of a discrete random variable, and provides the possible values and their associated probabilities. It is the function \[p:\mathbb{R}\to \left[ 0,1 \right]\] defined by \[p_{X}(x)=P(X=x)=P(\left\{ \omega\in \Omega\,\,\text{s.t.}\,\,X(\omega)=x \right\})\] for \[x=\left( -\infty,\infty \right)\] where \[P\] is a probability measure. The probability mass function must fulfil the properties \[\sum_{x}p_{X}(x)=1\] and \[p_{X}(x)\ge0\].

Note that for any set \[A\subset \mathbb{R}\], we can find the probability that \[X\in A\] with \[P(X\in A)=\sum_{x\in A}p_{X}(x)\].

Expected value

Let \[\mathcal{X}\] represent the support of some discrete random variable \[X\], or more precisely let \[\mathcal{X}=\left\{ x:p_{X}(x)>0 \right\}\].

The expected value (or simply the mean) of a probability mass function is then given as \[E(X)=\sum_{x\in \mathcal{X}} \left( x\cdot p_{X}(x) \right)\] on a finite sample space.